CGST Notification 82/2020

| Title | Seeks to make the Thirteenth amendment (2020) to the CGST Rules.2017 |

| Number | 82/2020 |

| Date | 10-11-2020 |

| Download | |

G.S.R……(E).-In exercise of the powers conferred by section 164 of the Central Goods and Services Tax Act, 2017 (12 of 2017), the Central Government, on recommendations of the Council, hereby makes the following rules further to amend the Central Goods and Services Tax Rules, 2017, namely:-

1.Short title and commencement. –(1) These rules may be called the Central Goods and Services Tax (Thirteenth Amendment) Rules, 2020.

(2) Save as otherwise provided in these rules, they shall come into force on the date of their publication in the Official Gazette.

2.In the Central Goods and Services Tax Rules, 2017 (hereafter in this notification referred to as the said rules), for rule 59,the following rule shall be substituted with effect from the 1stday of January, 2021 namely:-

“59.Form and manner of furnishing details of outward supplies.-(1) Every registered person, other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017(13 of 2017), required to furnish the details of outward supplies of goods or services or both under section 37, shall furnish such details in FORM GSTR-1for the month or the quarter, as the case may be, electronically through the common portal, either directly or through a Facilitation Centre as may be notified by the Commissioner.

(2) The registered persons required to furnish return for every quarter under proviso to sub-section (1) of section 39 may furnish the details of such outward supplies of goods or services or both to a registered person, as he may consider necessary, for the first and second months of a quarter, up to a cumulative value of fifty lakh rupees in each of the months,-using invoice furnishing facility (hereafter in this notification referred to as the “IFF”) electronically on the common portal, duly authenticated in the manner prescribed under rule 26, from the 1stday of the month succeeding such month till the 13thday of the said month.

(3) The details of outward supplies furnished using the IFF, for the first and second months of a quarter, shall not be furnished in FORM GSTR-1for the said quarter.

(4)The details of outward supplies of goods or services or both furnished in FORM GSTR-1shall include the–

(a) invoice wise details of all

(i) inter-State and intra-State supplies made to the registered persons; and

(ii) inter-State supplies with invoice value more than two and a half lakh rupees made to the unregistered persons;

(b) consolidated details of all-

(i) intra-State supplies made to unregistered persons for each rate of tax; and

(ii) State wise inter-State supplies with invoice value up to two and a half lakh rupees made to unregistered persons for each rate of tax;

(c) debitand credit notes, if any, issued during the month for invoices issued previously.

(5)The details of outward supplies of goods or services or both furnished using the IFF shall include the –

(a) invoice wise details of inter-State and intra-State supplies made to the registered persons;

(b) debit and credit notes, if any, issued during the month for such invoices issued previously.”

3. In the said rules, for rule 60, the following rule shall be substituted with effect from the 1stday of January, 2021, namely:-

“60.Form and manner of ascertaining details of inward supplies.-(1)The details of outward supplies furnished by the supplier in FORM GSTR-1 or using the IFF shall be made available electronically to the concerned registered persons (recipients)in Part A of FORM GSTR-2A, in FORM GSTR-4Aand in FORM GSTR-6A through the common portal, as the case may be.

(2) The details of invoices furnished by an non-resident taxable person in his return in FORM GSTR-5under rule 63 shall be made available to the recipient of credit in Part A of FORM GSTR 2A electronically through the common portal.

(3) The details of invoices furnished by an Input Service Distributor in his return in FORM GSTR-6under rule 65 shall be made available to the recipient of credit in Part B of FORM GSTR 2A electronically through the common portal.

(4) The details of tax deducted at source furnished by the deductor under sub-section (3) of section 39 in FORM GSTR-7shall be made available to the deductee in Part C of FORM GSTR-2A electronically through the common portal

(5) The details of tax collected at source furnished by an e-commerce operator under section 52in FORM GSTR-8 shall be made available to the concerned person in Part C of FORM GSTR 2A electronically through the common portal.

(6) The details of the integrated tax paid on the import of goods or goods brought in domestic Tariff Area from Special Economic Zone unit or a Special Economic Zone developer on a bill of entry shall be made available in Part D of FORM GSTR-2A electronically through the common portal

(7) An auto-drafted statement containing the details of input tax credit shall be made available to the registered person in FORM GSTR-2B,for every month, electronically through the common portal, and shall consist of –

(i) the details of outward supplies furnished by his supplier, other than a supplier required to furnish return for every quarter under proviso to sub-section (1) of section 39,in FORM GSTR-1, between the day immediately after the due date of furnishing of FORM GSTR-1for the previous month to the due date of furnishing of FORM GSTR-1for the month;

(ii) the details of invoices furnished by a non-resident taxable person in FORM GSTR-5and details of invoices furnished by an Input Service Distributor in his return in FORM GSTR-6and details of outward supplies furnished by his supplier, required to furnish return for every quarter under proviso to sub-section (1) of section 39,in FORM GSTR-1or using the IFF, as the case may be,-

(a) for the first month of the quarter, between the day immediately after the due date of furnishing of FORM GSTR-1for the preceding quarter to the due date of furnishing details using the IFF for the first month of the quarter;

(b) for the second month of the quarter, between the day immediately after the due date of furnishing details using the IFF for the first month of the quarter to the due date of furnishing details using the IFF for the second month of the quarter;

(c) for the third month of the quarter, between the day immediately after the due date of furnishing of details using the IFF for the second month of the quarter to the due date of furnishing of FORM GSTR-1 for the quarter;

(iii) the details of the integrated tax paid on the import of goods or goods brought in the domestic Tariff Area from Special Economic Zone unit or a Special Economic Zone developer on a bill of entry in the month.

(8)The Statement in FORM GSTR-2Bfor every month shall be made available to the registered person,

(i) for the first and second month of a quarter, a day after the due date of furnishing of details of outward supplies for the said month, in the IFF by a registered person required to furnish return for every quarter under proviso to sub-section (1) of section 39,orin FORM GSTR-1by a registered person, other than those required to furnish return for every quarter under proviso to sub-section (1) of section 39, whichever is later;

(ii) in the third month of the quarter, a day after the due date of furnishing of details of outward supplies for the said month, in FORM GSTR-1by a registered person required to furnish return for every quarter under proviso to sub-section (1) of section 39.”

4.In the said rules, in rule 61, after sub-rule (5), the following sub-rule shall be inserted, namely: –

“(6) Every registered person other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017(13 of 2017)or an Input Service Distributor or a non-resident taxable person or a person paying tax under section 10 or section 51 or, as the case may be, under section 52 shall furnish a return in FORM GSTR-3B,electronically through the common portal either directly or through a Facilitation Centre notified by the Commissioner, on or before the twentieth day of the month succeeding such tax period:

Provided that for taxpayers having an aggregate turnover of up to five crore rupees in the previous financial year, whose principal place of business is in the States of Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep, the return in FORM GSTR-3Bof the said rules for the months of October, 2020 to March, 2021 shall be furnished electronically through the common portal, on or before the twenty-second day of the month succeeding such month:

Provided further that for taxpayers having an aggregate turnover of up to five crore rupees in the previous financial year, whose principal place of business is in the States of Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi, the return in FORM GSTR-3Bof the said rules for the months of October, 2020 to March, 2021shall be furnished electronically through the common portal, on or before the twenty-fourth day of the month succeeding such month.”

5. In the said rules, for rule 61,the following rule shall be substituted with effect from the 1stday of January, 2021, namely: –

“61. Form and manner of furnishing of return.-(1) Every registered person other than a person referred to in section 14 of the Integrated Goods and Services Tax Act, 2017(13 of 2017)or an Input Service Distributor or a non-resident taxable person or a person paying tax under section 10 or section 51 or, as the case may be, under section 52 shall furnish a return in FORM GSTR-3B,electronically through the common portal either directly or through a Facilitation Centre notified by the Commissioner, as specified under –

(i) sub-section (1) of section 39,for each month, or part thereof, on or before the twentieth day of the month succeeding such month:

(ii) proviso to sub-section (1) of section 39,for each quarter, or part thereof, for the class of registered persons mentioned in column (2) of the Table given below, on or before the date mentioned in the corresponding entry in column (3) of the said Table, namely:–

Table

(2) Every registered person required to furnish return, under sub-rule (1) shall, subject to the provisions of section 49, discharge his liability towards tax, interest, penalty, fees or any other amount payable under the Act or the provisions of this Chapter by debiting the electronic cash ledger or electronic credit ledger and include the details in the return in FORM GSTR-3B.

(3) Every registered person required to furnish return, every quarter, under clause (ii) of sub-rule (1)shall pay the tax due under proviso to sub-section (7) of section 39, for each of the first two months of the quarter, by depositing the said amount in FORM GST PMT-06, by the twenty fifth day of the month succeeding such month:

Provided that the Commissioner may, on the recommendations of the Council, by notification, extend the due date for depositing the said amount in FORM GST PMT-06, for such class of taxable persons as may be specified therein:

Provided further that any extension of time limit notified by the Commissioner of State tax or Union territory tax shall be deemed to be notified by the Commissioner:

Provided also that while making a deposit in FORM GST PMT-06, such a registered person may –

(a) for the first month of the quarter, take into account the balance in the electronic cash ledger.

(b) for the second month of the quarter, take into account the balance in the electronic cash ledger excluding the tax due for the first month.

(4) The amount deposited by the registered persons under sub-rule (3) above, shall be debited while filing the return for the said quarter in FORM GSTR-3B, and any claim of refund of such amount lying in balance in the electronic cash ledger, if any, out of the amount so deposited shall be permitted only after the return in FORM GSTR-3Bfor the said quarter has been filed.”.

6.In the said rules, after rule 61, the following rule shall be inserted, namely:-

“61A.Manner of opting for furnishing quarterly return.-(1) Every registered person intending to furnish return on a quarterly basis under proviso to sub-section (1) of section 39, shall in accordance with the conditions and restrictions notified in this regard, indicate his preference for furnishing of return on a quarterly basis, electronically, on the common portal, from the 1stdayof the second month of the preceding quarter till the last day of the first month of the quarter for which the option is being exercised:

Provided that where such option has been exercised once, the said registered person shall continue to furnish the return on a quarterly basis for future tax periods, unless the said registered person,–

(a) becomes ineligible for furnishing the return on a quarterly basis as per the conditions and restrictions notified in this regard; or

(b) opts for furnishing of return on a monthly basis, electronically, on the common portal:

Provided further that a registered person shall not be eligible to opt for furnishing quarterly return incase the last return due on the date of exercising such option has not been furnished.

(2) A registered person, whose aggregate turnover exceeds 5 crore rupees during the current financial year, shall opt for furnishing of return on a monthly basis, electronically, on the common portal, from the first month of the quarter, succeeding the quarter during which his aggregate turnover exceeds 5 crore rupees.

7. In the said rules, in rule 62,

(i) in sub-rule (1),the words, figures, letters and brackets“ or paying tax by availing the benefit of notification of the Government of India, Ministry of Finance, Department of Revenue No. 02/2019–Central Tax (Rate), dated the 7th March, 2019, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R.189 (E), dated the 7th March, 2019” shall be omitted;(ii)in sub-rule (4), the words, figures, letters and brackets “or by availing the benefit of notification of the Government of India, Ministry of Finance, Department of Revenue No. 02/2019–Central Tax (Rate), dated the 7th March, 2019, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R.189 (E), dated the 7th March, 2019”shall be omitted;

of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R.189 (E), dated the 7th March, 2019”shall be omitted;

(iii) in the explanation to sub-rule (4), the words, figures, letters and brackets “or opting for paying tax by availing the benefit of notification of the Government of India, Ministry of Finance, Department of Revenue No. 02/2019–Central Tax (Rate), dated the 7th March, 2019, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R.189 (E), dated the 7th March, 2019.”shall be omitted;

(iv) sub-rule (6) shall be omitted.

7. In FORM GSTR-1, in the Instructions, after serial number 17, the following instruction shall be inserted, namely:-

“18. It will be mandatory to specify the number of digits of HSN code for goods or services that a class of registered persons shall be required to mention as may be specified in the notification issued from time to time under proviso to rule 46 of the said rules.

8. After FORM-2A, the following FORM shall be inserted, namely: –

“FORM-2B

[See rule 60(7)

Auto-drafted ITC Statement

(From FORM GSTR-1, GSTR-5, GSTR-6 and Import data received from ICEGATE)

3. ITC Available Summary

4. ITC Not Available Summary

Instructions:

1.Terms Used :-

a. ITC –Input tax credit

b. B2B –Business to Business

c. ISD –Input service distributor

d. IMPG –Import of goods

e. IMPGSEZ –Import of goods from SEZ

3. It may be noted that FORM GSTR-2Bwill consist of all the FORM GSTR-1s, 5s and 6sbeing filed by your suppliers, generally between the due dates of filing of two consequent GSTR-1 or furnishing of IFFs, based on the filing option (monthly or quarterly) as chosen by the corresponding supplier. The dates for which the relevant data has been extracted is specified in the CGST Rules and is also available under the “View Advisory” tab on the online portal. For example, FORM GSTR-2Bfor the month of February will consist of all the documents filed by suppliers who choose to file their FORM GSTR-1monthly from 00:00 hours on 12thFebruary to 23:59 hours on 11thMarch.

4. It also contains information on imports of goods from the ICEGATE system including data on imports from Special Economic Zones Units / Developers.

5. It may be noted that reverse charge credit on import of services is not part of this statement and will be continued to be entered by taxpayers in Table 4(A)(2) of FORM GSTR-3B.

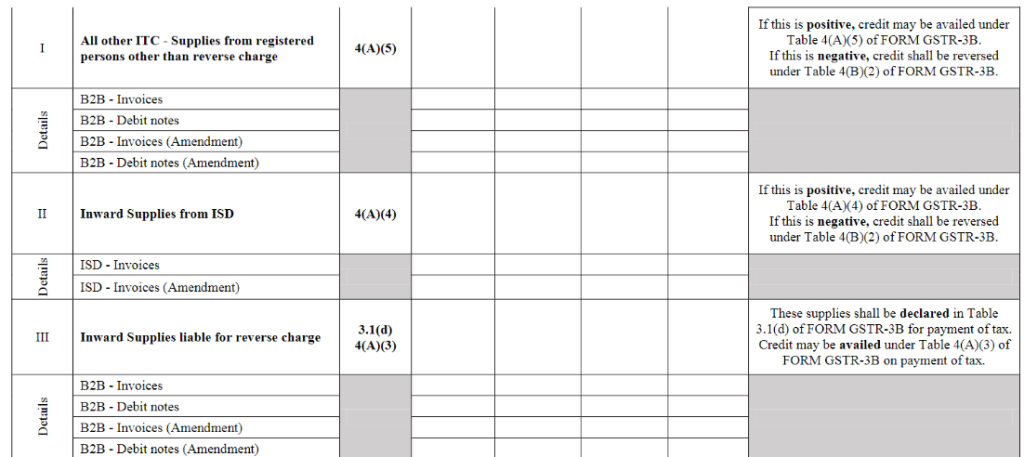

6.Table 3 captures the summary of ITC available as on the date of generation of FORM GSTR-2B. It is divided into following two parts:

A. Part A captures the summary of credit that may be availed in relevant tables of FORM GSTR-3B.

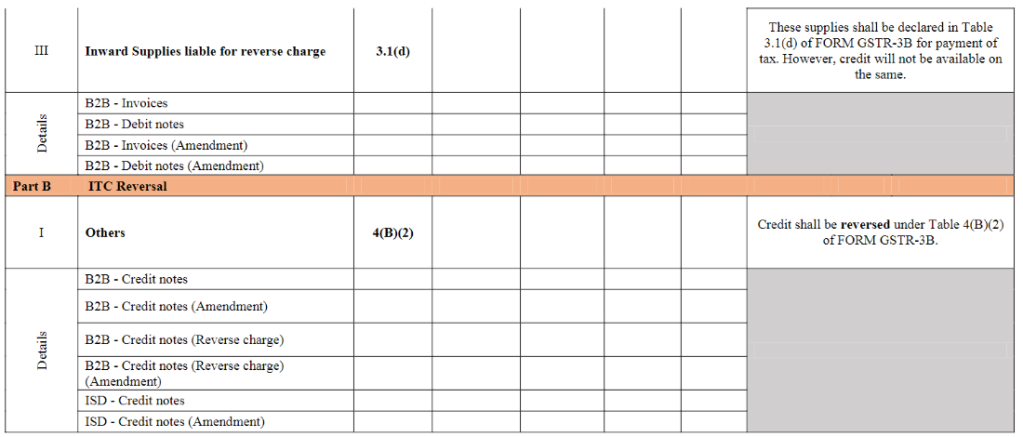

B. Part B captures the summary of credit that shall be reversed in relevant table of FORM GSTR-3B.

7. Table 4 captures the summary of ITC not available as on the date of generation of FORM GSTR-2B. Credit available in this table shall not be availed as credit in FORM GSTR-3B. However, the liability to pay tax on reverse charge basis and the liability to reverse credit on receipt of credit notes continues for such supplies.

8. Taxpayers are advised to ensure that the data generated in FORM GSTR-2Bis reconciled with their own records and books of accounts. Tax payers shall ensure that

a. No credit shall be taken twice for any document under any circumstances.

b. Credit shall be reversed wherever necessary.

c. Tax on reverse charge basis shall be paid

9. Details of invoices, credit notes, debit notes, ISD invoices, ISD credit and debit notes, bill of entries etc. will also be made available online and through download facility.

10. There may be scenarios where a percentage of the applicable rate of tax rate may be notified by the Government. A separate column will be provided for invoices / documents where such rate is applicable.

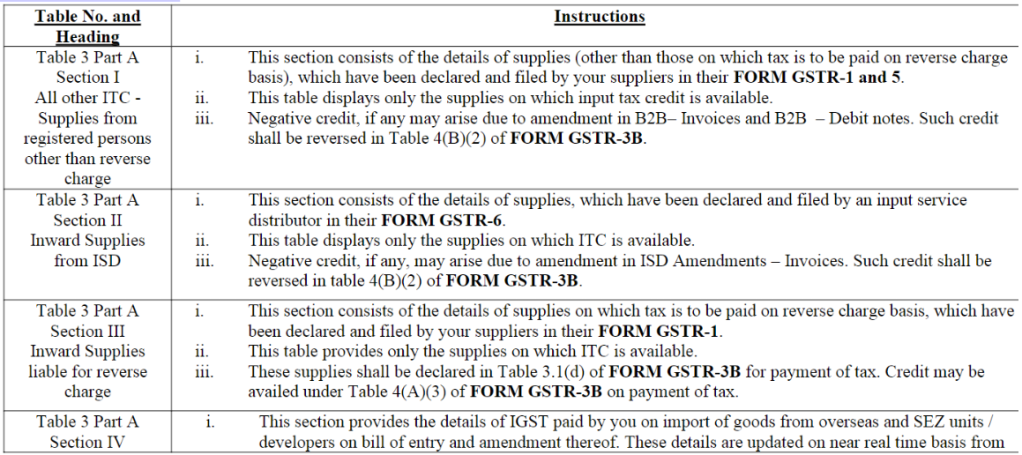

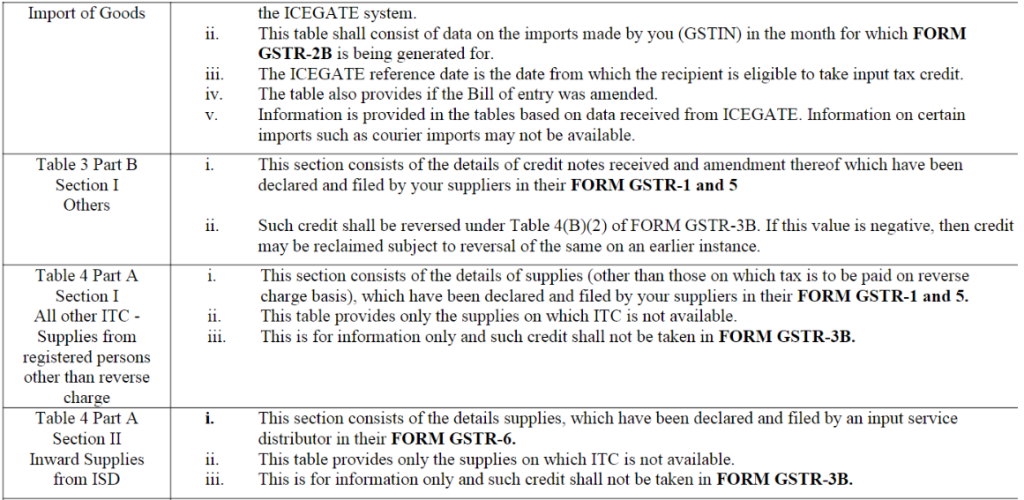

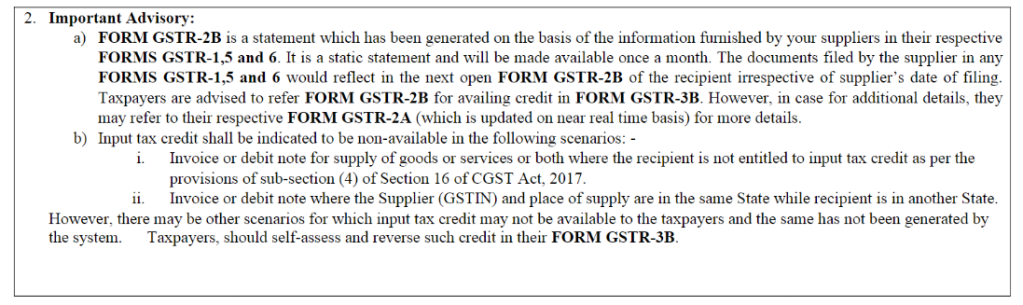

11.Table wise instructions: